Useful Information

Social Security: Now or Later?

Delaying benefits will increase the size of your checks, but it's not the best strategy for everyone.

Many financial planners, as well as Kiplinger, recommend waiting until at least your full retirement age--or, even better, until you're 70--to claim Social Security. You're eligible to file for Social Security as early as age 62, but if you do, your benefits will be permanently reduced by at least 25%. Waiting until full retirement age--66 for most baby boomers--means you'll receive 100% of the benefits you've earned. And if you continue to postpone filing for benefits after you reach full retirement age, your payouts will grow by 8% a year until you reach age 70.

SEE ALSO: 10 Things You Must Know About Social Security

That, combined with cost-of-living adjustments in most years, is a return you're unlikely to get anywhere else. Yet retirees seem to be ignoring those numbers: Nearly 60% of retirees claim benefits before age 66, and about one-third of those retirees claim benefits at 62. Are they misguided or onto something?

Figuring out when to file for Social Security usually comes down to a question that's nearly impossible to answer: How long will you live? Retirees who wait until full retirement age or later will receive fewer checks over their lifetime, but the checks will be for larger amounts. The longer you live, the more delaying pays off.

Do the math

The age at which you come out ahead by postponing benefits is known as your break-even age. For example, a 62-year-old top wage earner would come out ahead by filing at 66 as long as he lives past age 77. If he delays filing for benefits until age 70, he would need to live past age 80 to break even. That's below the average life expectancy (84 for men and nearly 87 for women), but if you don't expect to live that long, there's no point in postponing your benefits.

However, if your grandmother celebrated her 100th birthday by playing a few rounds of golf, and you're fit and healthy, you're probably better off waiting until at least full retirement age--or, better yet, age 70--to file your claim.

If you're married--even if your own health or your family history suggests you won't reach your break-even age--there's another factor to consider: survivor benefits. For example, if you're the higher earner and you die first, your spouse will be able to take over your benefits. Delaying benefits will boost the monthly benefit your spouse will receive after you're gone.

Single retirees are usually better off waiting until full retirement age to file for Social Security. But because you don't have to worry about survivor benefits--your benefits will end when you do--you have a less-compelling reason to wait until age 70 to file. Your decision will come down to how badly you need the income and how long you think you'll live.

It's usually not a good idea to claim benefits before full retirement age if you're still working. In 2019, Social Security will temporarily withhold $1 of your benefits for every $2 you earn over $17,640 if you haven't reached full retirement age. If you'll reach the magic number in 2019, it will withhold $1 for every $3 over $46,920 in earnings in the months before you hit full retirement age. After that, you don't have to worry about the earnings test.

Invest your benefits?

Before 2010, retirees who filed for benefits at age 62 and later changed their mind could withdraw their application for benefits, repay the total amount they had received and reapply for a higher benefit based on their age. Now, if you want to withdraw your application for Social Security and repay benefits, you must do it within 12 months after signing up, and you can only do it once. You still have the option of suspending benefits at full retirement age, which will allow you to accrue the 8% delayed retirement credit until age 70.

Even with the payback option eliminated, some retirees remain convinced that they can come out ahead by filing at 62 and investing their benefits. That way, they argue, they won't leave money on the table if they die before their break-even age. This strategy also appeals to retirees who fear that a shortfall in the Social Security trust fund will force the government to cut future benefits.

But in order to beat the guaranteed return you would get by delaying benefits (plus cost-of-living increases), you'd need to invest most of your benefits in stocks, financial planners say. That could work out in your favor--but if the market turns bearish, you won't have years to recover your losses, says Gifford Lehman, a certified financial planner in Monterey, Calif.

Even in the best of times, this game plan requires you to resist the temptation to spend your monthly Social Security check, says Jim Blankenship, a CFP in New Berlin, Ill. "The reality is that many, if not most, folks don't have the discipline to invest the money, and before you know it the projected windfall from filing early has been eaten up by lifestyle creep," he says.

What about worries that Social Security won't be around if you wait? Barring congressional action, the trust fund is slated to run out of money in 2034. It's unlikely, though, that Congress will do nothing over the next 15 years to fix Social Security (see Relax, Your Social Security Benefits Are Safe). And at that point, payroll taxes would still fund 79% of promised benefits. Any actions Congress takes to shore up the trust fund probably won't affect current retirees.

How to bridge the gap

Some retirees file for Social Security before full retirement age because they're reluctant to tap their retirement plans. Filing for Social Security benefits early may allow you to postpone taking money out of savings, but that strategy may cost you more in the long run.

SEE ALSO: Do You Know the Best Social Security Claiming Strategies?

Here's why: Once you turn 70½, you must withdraw required minimum distributions from all of your tax-deferred retirement plans, based on your life expectancy and the balance in those plans at year-end. Leaving those accounts untouched until you turn 70½ will increase the size of mandatory withdrawals, along with your tax bill. Depending on your other income, you could find yourself vaulted into a higher tax bracket. Large RMDs could also trigger taxes on up to 85% of your Social Security benefits, plus a surcharge on your Medicare Part B and Part D premiums.

By taking withdrawals from your retirement plans before you hit your seventies, you can reduce the size of those accounts, which will result in smaller taxable RMDs, says Cindi Hill, a certified financial planner with CUNA Mutual Group. You can take money from your tax-deferred accounts with a fairly high degree of confidence that your savings will last 30 years or more--through bear markets and bouts of inflation--if you follow the "4% rule" as a starting point. In your first year of retirement, you withdraw 4% from savings, and you increase the dollar amount of your subsequent annual withdrawals by the previous year's inflation rate (see Make Your Money Last). You may decide to dial back withdrawals once you start taking Social Security benefits, but the rule is a good starting point.

While this strategy is designed to ensure that you won't outlive your money, it's not bulletproof. During the 2008 economic downturn, some retirees were forced to withdraw money from depressed portfolios, inflicting permanent damage to their savings. In that scenario, filing for Social Security benefits before age 70 could enable you to postpone withdrawals until your investments have recovered. Cary Cates, a CFP in Denton, Texas, says he often advises clients to plan on filing for benefits at age 70 but to be prepared to file earlier if their investment portfolio suffers a significant decline. "This reduces the need to sell securities when the value is depressed," he says.

Another way to protect yourself from market downturns is to use an immediate annuity to cover your expenses until you file for benefits. Suppose you're 65 but want to wait until you're 70 to claim benefits--and that claiming now would provide $2,093 a month in benefits. For about $120,650, you could buy an annuity that provides the same amount each month for five years, at which point you would file for Social Security.

Thanks to estimated cost-of-living adjustments and the 8% delayed retirement credit, your benefits would be worth more than $3,600 a month. If you live until at least age 83, you'll come out ahead. You can shop for an immediate annuity and compare rates at immediateannuities.com.

Maximizing benefits

If you are (or were) married

For married couples, claiming benefits "is a household decision, not an individual decision," says Paula McMillan, a certified financial planner in Greensboro, N.C. Under a couple of scenarios, it makes sense for one spouse (or widowed spouse) to claim benefits before full retirement age.

You're the lower-earning spouse. If you were born on or before January 1, 1954, you can still take advantage of a strategy known as restricting an application to increase the combined payout of your benefits as a couple. Here's an example of how it works: One spouse files for Social Security benefits before full retirement age, while the other--who must have already reached full retirement age--files a restricted application to collect spousal benefits only, which are equal to half of the first spouse's full benefits. The second spouse waits until 70 to collect his or her own benefit, thus taking advantage of delayed retirement credits.

Even if you're ineligible for that strategy, it may make sense for the lower-earning spouse to file as early as age 62, says Blankenship. While that spouse will see a 25% reduction in benefits, the couple can use income from the lower-earning spouse's benefits, along with other sources of income, to pay expenses, enabling them to delay the higher earner's benefits until age 70.

You're eligible for survivor benefits. You can file for Social Security based on your late spouse's earnings as early as age 60 (50 if you're totally disabled). Your benefits will be based on your deceased spouse's benefits when he or she died. If your spouse died before filing, your payout will be based on the amount your spouse would have earned at full retirement age.

To receive 100% of your late spouse's benefit, you must wait until your own full retirement age to file; otherwise, it will be reduced by a certain amount for every month you file your claim before your full retirement age. But whether you wait until full retirement age or file earlier, claiming survivor benefits won't affect your own payout. Claiming survivor benefits--even if they're smaller than your own--allows your own benefits to continue to grow. At age 70, you can switch to your own benefits, which will have been enhanced by the delayed retirement credit.

SEE ALSO: Social Security for Divorcees

Survivor benefits are also available to divorced spouses whose former spouses have passed away, although many don't realize they're eligible, says Jayson Owens, a CFP in Anchorage, Alaska. If you were married for at least 10 years, you can claim benefits as early as age 60 based on your late ex's earnings record. As is the case with surviving spouses, this strategy offers a way to postpone claiming your own benefits until age 70, Owens says. Remarriage won't affect your eligibility for survivor benefits as long as you're at least 60 years old (50 if you're totally disabled).

The Social Security Retirement Age Increases to 66.5 in 2019

Emily Brandon,U.S.News & World Report 20 hours ago

-

Email

While you can start Social Security payments at age 62, your monthly checks are reduced if you begin collecting benefits at this age. To claim your full benefit you need to sign up for Social Security at your full retirement age, which varies by birth year. Here's a look at how the retirement age is changing, and what this means for your retirement payments.

An older Social Security full retirement age. The full retirement age used to be 65 for those born in 1937 or earlier. Those born between 1943 and 1954 have a full retirement age of 66. The full retirement age further increases to 66 and six months for people born in 1957, up from 66 and four months for those with a birth year of 1956. "The full retirement age increases for those born in 1957 who attain age 62 in 2019," says Jim Blair, a former Social Security administrator and lead consultant at Premier Social Security Consulting in Cincinnati, Ohio. "Full retirement age is 66 years, six months. This is a two-month increase over those born in 1956." The full retirement age will further increase in two-month increments each year until it hits 67 for everyone born in 1960 or later.

[Read: Social Security Changes Coming in 2019.]

A bigger reduction if you claim Social Security early. Workers who are eligible for Social Security can start payments at age 62, regardless of their full retirement age. However, the benefit reduction for early claiming is bigger for those who have an older retirement age. "Your Social Security full retirement age -- the age where you get a 100 percent benefit -- is based on your birth year," says Andy Landis, author of "Social Security: The Inside Story." "For those born in 1957, your full retirement age is 66 and six months. You can still get payments as early as 62, at 72.5 percent of your full payment amount."

Workers born in 1957 will see their monthly payments reduced by 27.5 percent if they sign up for Social Security at age 62, compared to a 26.67 percent benefit reduction for those born in 1956 and a 25 percent decrease for those born in 1954. For a worker eligible for a $1,000 monthly Social Security benefit at his full retirement age, claiming at age 62 will reduce his monthly payment to $750 if his birth year is 1954 and $725 if he was born in 1957. "Relative to an earlier full retirement age, a later full retirement age means that the person gets less money per month, regardless of when they file," says Mike Piper, a certified public accountant and author of "Social Security Made Simple." Social Security's annual cost-of-living adjustments will be applied to these reduced payments, resulting in a smaller dollar value of the inflation adjustments as well.

[Read: How Much You Will Get From Social Security.]

Less of a benefit for delaying claiming Social Security. You can increase your monthly Social Security payments by delaying claiming Social Security after your full retirement age up until age 70. However, those who have an older retirement age have fewer months to delay claiming Social Security and less of an opportunity to earn delayed retirement credits. "If a person files at age 70, if they had a full retirement age of 66, that means they waited 48 months beyond full retirement age, so they would get 132 percent of their primary insurance amount," Piper says. "But if they file at 70 with a full retirement age of 66 and six months, that means they waited 42 months beyond full retirement age, so they would only get 128 percent of their primary insurance amount."

The Medicare eligibility age remains the same. While the Social Security full retirement age has increased over the past several years, the age when workers qualify for Medicare has remained age 65. Those who delay claiming Social Security until their full retirement age or later still need to sign up for Medicare at age 65 or maintain other group health insurance based on current employment to avoid hefty Medicare late enrollment penalties. While many retirees have their Medicare premiums withheld from their Social Security checks, those who enroll in Medicare before starting Social Security will have to pay premiums out of pocket.

[See: 10 Ways to Increase Your Social Security Payments.]

Carefully determine the optimal age to start Social Security. Your age when you begin Social Security payments plays a big role in the amount you will receive throughout retirement. But regardless of your birth year, there are several ways to boost your monthly Social Security payments including delaying claiming, continuing to work and coordinating benefits with a spouse. "When to claim benefits should be something that people take the time to analyze and make sure they know the impact of their decision," says Angie Furubotten-LaRosee, a certified financial planner at Avea Financial Planning in Richland, Washington. "By delaying to at least full retirement age, right now between 66 and 67, or even delaying until age 70, people can increase the amount they will receive."

Are You Making These 4 Major 401(k) Mistakes?

If you're lucky enough to have access to an employer-sponsored 401(k), you should know that you have a great opportunity to accumulate a bundle in time for retirement. That's because 401(k)s allow you to contribute much more on an annual basis than IRAs. The current yearly limits are $18,500 for workers under 50 and $24,500 for those 50 and over. By comparison, IRAs max out at $5,500 and $6,500 a year, respectively.

Still, having a 401(k) will only get you so far if you don't manage it wisely. With that in mind, here are a few major mistakes you should make every effort to avoid.

1. Not contributing enough to snag your employer's match

One benefit of having a 401(k) is the opportunity to build wealth not just with your own money but your employer's as well. In fact, 92% of companies that offer a 401(k) also match worker contributions to some degree. But to get that money, you'll need to contribute money of your own. Unfortunately, an estimated 25% of workers don't put in enough to capitalize fully on their employers' matching dollars, and are thus leaving a collective $24 billion on the table each year.

If you're not getting your employer match, you're kissing free money goodbye — so don't let that continue. Figure out how much you need to put into your 401(k) to get that match, and cut corners in your budget to make up for a slightly smaller paycheck. Otherwise, you'll miss out on not just your company match itself, but the potential to invest it and grow it into a larger sum over time.

2. Not increasing your contributions year after year

Many workers get a raise year after year. If you're one of them, then you're doing yourself a major disservice by not sticking that extra money into your 401(k) before it shows up in your paychecks.

Think about it: Unless your expenses go up drastically from year to year, you can probably get by without that additional money. So, if you arrange to have it land in your 401(k) from the start, you won't come to miss it.

3. Sticking with your plan's default investment

When you first sign up for a 401(k), you'll be automatically invested in your plan's default option until you select your own investments. That default option is usually a target date fund, and while that may be a good choice for some workers, it's not necessarily the best choice for you.

Target date funds are designed to grow increasingly conservative as their associated milestones near. For example, if you invest in a target date fund for retirement over a 30-year period, you'll generally start out with a more aggressive investment mix and will shift toward safer assets as that period winds down.

The problem with target date funds is that they don't necessarily provide the best returns on investment, nor is your 401(k)'s default target date fund designed to align with your specific strategy or tolerance for risk. A better bet, therefore, is to review your plan's investment options and choose those that are more likely to help you meet your goals. Keep in mind that you may, after reviewing your choices, decide to stick with that default fund, and that's fine. Just don't make the mistake of not exploring alternatives first.

4. Not paying attention to investment fees

Of the various investments you'll get to choose from in your 401(k), some are bound to be more expensive than others. But if you don't pay attention to fees, you could end up losing thousands upon thousands of dollars in your lifetime without being any the wiser. The funds in your 401(k) are required to disclose their associated fees, so take a look at those numbers and aim to keep them as low as possible without compromising on returns. You can generally pull this off by sticking mostly to index funds, which are passively managed and don't have the same costs as actively managed mutual funds.

Participating in a 401(k) plan is a great way to set yourself up for a comfortable retirement. Avoiding these mistakes will help you make the most of that plan, leaving you with a higher ending balance by the time your golden years eventually roll around.

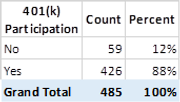

MIT and Lincoln Laboratory 401k Participation

Take advantage of your 401k benefit!

100% of Draper Members participate in their Retirement Plan!

47% of American Pre-Retirees Failed This Basic Social Security Quiz - Can You Pass It?

You get a passing grade if you can get four of these five true/false questions correct:

-

Under current Social Security law, my benefits will not be reduced if I claim them at age 65.

-

My spouse is eligible to receive Social Security retirement benefits, even if he or she has no individual earnings history.

-

If my spouse dies, I will continue to receive both my own benefit and my deceased spouse's benefit; the total Social Security benefits I receive will not change.

-

Social Security retirement benefits are based on my earnings history; I'll receive the same monthly benefit amount whether I start collecting before or after my full retirement age.

-

If I am still working when I claim my Social Security, my benefit might be reduced, depending on my earnings and my age.

Done? See the answers . Regardless of how you scored, remember that we're proud of you no matter what.

Cool Labor Site: Labor Council for Latin American Advancement

The Labor Council for Latin American Advancement (LCLAA) is a national organization representing the interests of approximately 2 million Latino/a trade unionists throughout the United States and Puerto Rico. With 65 Chapters, LCLAA members engage in different creative programs that promote political empowerment, cultural pride, and economic development of Latino workers and their families. http://www.lclaa.org/

Cool Labor Book: Unions and the City

Edited by Ian Thomas MacDonald

“Urban space offers allies and political leverage to unions, even as it creates tensions and fractures that unions do not necessarily intend or foresee. Often, labor strategies succeed in trade union terms without pointing the way to the renewal that labor movements in North America desperately need... Can we nevertheless treat these strategies as promising experiments...?” —From the Introduction to Unions and the City: Negotiating Urban Change.

—This item and the books featured in this newsletter are available at http://www.laborbooks.com.

Cool Labor Book: Welcome to the Union — A Pamphlet for New Employees

(Two versions: Private Sector or Public Sector)

By Michael Mauer

Don’t let management’s voice be the only one heard by new employees who hire on in your unionized workplace. Welcome them to the job with this easy-to-read, solidarity-building introduction to unionism. It comes in two versions—public sector and private sector.

Welcome to the Union helps new co-workers understand unionism and is designed to win their support and involvement. It’s a quick and easy read that offers a concise, to-the-point explanation of how unions operate and the vital role every employee can play helping improve the workplace for all. Published by UCS. Inquire about discounts for larger orders and/or imprinting your union logo. Please specify Public or Private sector in the comment field when ordering.

—This item and the books featured in this newsletter are available at http://www.laborbooks.com.